By Chris Stephen

The capture of the country’s four central oil ports by the army of general Khalifa Hafter in September has seen oil production almost double, and brought the subsequent re-opening of abandoned fields by the National Oil Corporation (NOC) in the Sirte basin.

The capture of the country’s four central oil ports by the army of general Khalifa Hafter in September has seen oil production almost double, and brought the subsequent re-opening of abandoned fields by the National Oil Corporation (NOC) in the Sirte basin.

It has also created a mass of opportunities for repair and maintenance work. But a bonanza it isn’t-not yet, anyway.

Foreign companies wanting to deploy to Libya face hefty political and security hurdles. Until the political turmoil dies down, only the brave will venture forth into a country where energy installations lie within striking distance of Islamic State (IS) and remain a potential battleground between Libya’s rival armed factions.

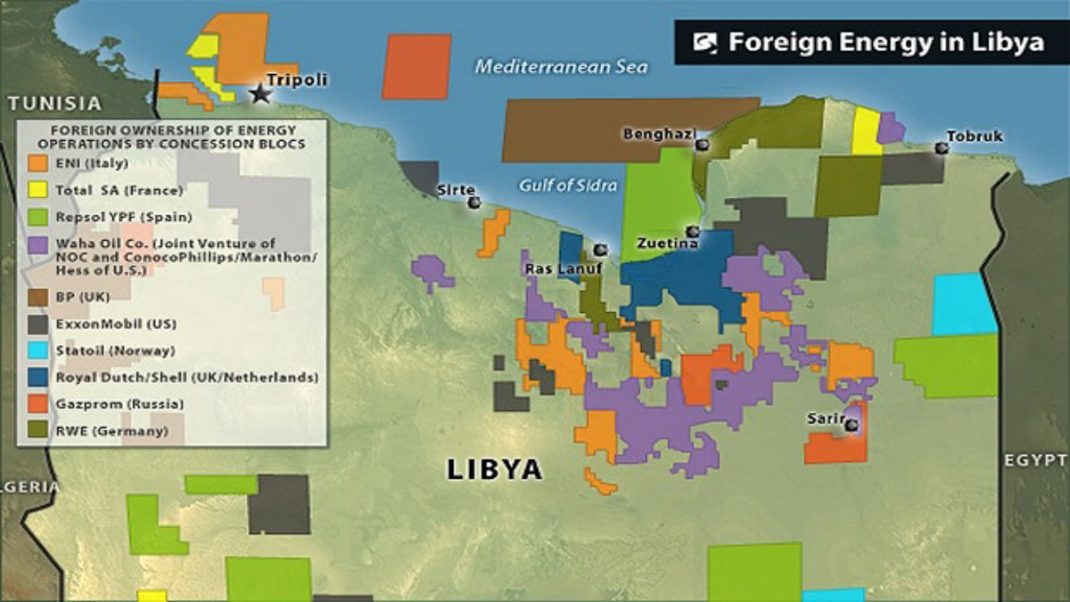

Hafter, commander of the forces of the Tobruk-based parliament, the House of Representatives (HoR), struck without warning on 11 September. Within three days, his Libyan National Army (LNA) was in control of: the 447,000-barrels-a-day-capacity Es Sider terminal (operated by National Oil Company, or NOC), NOC’s 220,000-b/d Ras Lanuf refining and export terminal, Zueitina’s 200,000-b/d port (a venture between NOC, Occidental and OMV) and NOC’s 51,000-b/d Brega refining and export facility. It was a sound defeat for the Petroleum Facilities Guard, a militia loyal to Tobruk’s rival in Tripoli, the UN-backed Government of National Accord (GNA).

The LNA already controlled the Sirte basin’s territory, home to two-thirds of Libya’s production, and the capture of the ports has brought the area and its energy facilities, for the moment, under singular authority.

The offensive also won the backing of NOC chairman Mustafa Sanallah, and by late November the country’s production had jumped from August’s 270,000 b/d to around 0.528m b/d.

Germany’s Wintershall has resumed output at its Concession 96 field, producing 35,000 b/d, and in early October NOC’s Benghazi-based unit, Arabian Gulf Oil Company(Agoco), increased output from the southeastern Sarir fields. Alongside the nearby Misla field, they are now pumping around 320,000 b/d.

Further growth will depend on two developments: a resumption of production from the Sharara and El Feel fields in the southwest, and repairing infrastructure in the Sirte basin. The former depends on politics-resolving the stand-off between the Zintani militias, loyal to the eastern government, which have blocked the pipelines from the fields, and local Misrata-loyal rivals, which control the fields themselves. But the fields and infrastructure in the west remain relatively healthy.

The Sirte basin is another story. It was Libya’s productive heartland, accounting for 0.6m b/d of the 1.6m b/d Libya produced before the 2011 civil war. Sanallah visited the re-captured Es-Sider and Ras Lanuf facilities in October and said remedial work there-including to pipelines and storage facilities at the terminals-would help lift the country’s output to 0.95m b/d by the end of the year. He told Petroleum Economist recently that NOC engineers were now at the facilities and able to resume work. Still, the damage has been significant and it’s unclear that NOC can repair everything itself, hampered by a tiny budget.

Labouring on

That should be a good signal for services firms. The rewards of patching up the area’s energy infrastructure would be great-allowing Libya to hone in on Sanallah’s near-1m-b/d target.

Sustaining that level, or increasing production beyond 1m b/d, will demand substantial repairs to abandoned wells, pipelines and ports damaged by war and neglect. Indeed, the NOC’s chairman says conflict since 2011 has reduced Libya’s technical capacity from 1.6m b/d to 1.2m b/d.

What can investors hoping to help patch up Libya’s oil sector expect? First, the good news. NOC, holding company for all Libya’s state oil assets, is the country’s best-run institution. Sanallah has earned a reputation as an open and friendly salesman for Libya’s potential too. His company has well-developed plans for fixing four key categories of plant; ports, pipelines, pumps and power generation-the four Ps.

Start with the ports. Es-Sider, the largest, and nearby Ras Lanuf, the country’s biggest (but still offline) refinery, sustained heavy damage in attacks in December 2014 by Misratan militias. Further attacks by IS terrorists in January this year caused more damage. All told, 17 storage tanks have either been destroyed or rendered inoperable. Fixing them is essential if output is to rise as NOC plans.

“You’ve got to have the terminals functioning again-you need to have the tanks. That’s the first problem,” says John Hamilton, director of London-based Cross Border Information. “It’s the most basic infrastructure problem.”

NOC lifted its force majeure-in place since December 2014-on the terminals in September, following the LNA’s capture of the facilities. Sanallah, though, says combined throughput capacity is at present about 200,000 b/d, or a third of 2011’s level.

The pipelines reaching the ports are the other problem. Assessing the extent of the damage may take some time. On paper, the pipes and their pumping stations can process more than 1m b/d from across the basin, but some will need cleaning and repairs carried out.

Surface facilities at some installations in the basin, like those at Total’s Mabruk field, have been destroyed. In some parts of the country, Libya’s waxy crude causes problems when the pipelines are left idle-turning them into the “longest candles in the world”, as an oilman in the country once described it. So there’s plenty of work for service firms.

Libyan oil doesn’t flow freely to the surface either. Pumping and injection is often needed, using equipment that needed to be replaced even before the start of the eight-month civil war in 2011. That equipment has lain dormant since then. Together with new or repaired pumps, many fields have been denuded of equipment including vehicles, base camps, fresh-water supply and accommodation blocks. That’s an opportunity for outside logistics companies and project managers.

Power generation remains the Achilles’ heel of Libya’s oil industry, as low national output obliges it to compete with rising domestic demand. Chronic power shortages already caused long blackouts and misery in Tripoli and southern towns, which will affect those fields sharing supplies with domestic customers.

In November, power failures at Waha Oil Company’s al-Dafa and Samah oilfields, in the Sirte basin, knocked out around 70,000 b/d of production. It was more than a one-off: electricity supply has also periodically hampered Agoco’s workhorse fields at Sarir too. The whole electricity-supply chain needs upgrading.

A 2014 deal signed by UK-based APR Energy to supply 450 megawatts has gone nowhere. No replacement is on the horizon.

Sanallah says NOC needs $2bn, on its own, to invest in upgrading its energy sector. That seems modest. NOC holds a 50% stake in most projects, so investors could be counted on to add to that total. Indeed, for foreign firms taking a purely technical view of Libya’s potential, the opportunity is plain.

“There’s going to be a lot of opportunity for maintenance, suppliers of equipment-that’s your basic starting point,” says Hamilton. “Moving on, there will be a demand for reservoir management, power supply, development projects, expanding existing resources to get more out of them.”

But that’s all on paper. The biggest problem facing investors is security. To begin with, the civil war is far from over. The UN-backed GNA has been unable to exert its authority over the country, despite continued support from international powers.

Although the LNA handed over technical, if not territorial, control of the Sirte basin’s energy infrastructure to NOC-a move that allowed for the rise in production this autumn-the GNA has demanded that it take full control of the facilities.

Hafter, who has talked of liberating Tripoli from the Islamist militias that allow the GNA to remain in the city, is unlikely to do that. So, if the GNA, which has no army of its own, is to wrest control from the LNA it must rely on Misratan forces opposed to Hafter.

That’s difficult for now, because Misrata’s biggest militia is deployed 100km from Es-Sider, and its units are tied-up battling IS in Sirte, backed by US air strikes. If, as expected, IS is defeated, the GNA and its Misratan loyalists may be tempted to move on the LNA-controlled ports and fields. Already, the GNA’s defence minister, Al-Mahdi al-Barghathi, a foe of Hafter’s, is thought to be amassing some troops to face down the LNA.

More mundanely although the NOC supported Hafter’s capture of the Sirte basin, the GNA itself, which has legal title to Libya’s oil revenues, has not. That makes it less willing to hand NOC the money it says it needs to carry out remedial work.

Complicating things further, the HoR’s prime minister, Abdullah al-Thinni, insists that Libya’s hard-currency oil-revenue earnings be split between the two governments, rather than, as now, flow exclusively to the GNA-controlled Central Bank of Libya in Tripoli.

This dispute has lingered for months-and Tobruk, which is now in control of all Libya’s oil-producing territory, could always return to the blockade of eastern ports it imposed for three weeks in May.

The stalemate between the two governments hasn’t been helped by the efforts of Islamists that controlled the rump General National Congress (GNC) to reinstate themselves in Tripoli, at the GNA’s expense. A coup attempt in October largely failed. Yet Khalifa Ghwell, a GNC leader before it was replaced by the GNA, remains in the capital, still trying to draw support from Islamists wishing to regain Tripoli and oppose Hafter.

None of this is compatible with the kind of stability that will bring in the investment needed in the country’s oil sector. “Before committing new capital investment to Libya, independent oil companies will want to see a durable political agreement, functioning government institutions and the restoration of security-all currently a long way off,” says Martijn Murphy, research manager at Wood Mackenzie, a consultancy.

“Libya’s national oil company will also have to secure funding for its 50% stake that it has in most projects, or fund its share with crude in kind.”

That too is increasingly doubtful. Although oil exports have risen sharply in recent months, the World Bank said in October that oil income could no longer meet Libya’s spending needs. Foreign reserves are running down and the economy was close to collapse, it said. Even if the GNA were minded to beef up NOC’s balance sheet, it would struggle to do so.

International investors will also remain wary of threats to personnel. Kidnapping and banditry are rife.

Governance is, to put it mildly, shaky.

“There are likely some contractors that will start to go back to Libya, says Geoff Porter, head of US North Africa Risk Consulting. But the risks are significant.

“There is the persistent ambient kidnapping risk, and one key commercial risk is getting paid for services rendered. Even if companies use letters of credit to mitigate against non-payment, there are numerous instances in the last two years where letters of credit have been altered by Libyan parties to effectively render them void.”

***

Chris Stephen – Libya Correspondent, The Guardian. Author, Judgement Day: The Trial of Slobodan Milosevic (Atlantic Monthly Press, New York)

_________________

Petroleum Economist